Rent vs. Buy -- math now favors Rent

-

I'm wrestling with this right now. I want to move to a nearby city, but have a great rate on my current house. So I'm leaning towards renting my current house out (I wouldn't break even, but close).

Still deciding if I should buy or rent the next house. Rent on a the next house seems like it'll be in the same ballpark as interest on a mortgage. Inventory on houses for sale where I'm looking is abysmal, I could rent for a few years, build a bigger downpayment and reassess. We'll see...

-

Couldn't read, due to paywall

Surely anybody who reads the Wall Street Journal can pay cash for their house?

I was only joking

-

AN extreme example i recently saw was in Bangkok (I know I know, apple vs. orange). But I was walking around and came across a condo development, so went in to take a look. Got a very nice tour of the whole building, including facilities, etc. Starting price for the ones they had left was 33,000,000 baht (about USD$1MM). However, you could rent a one bedroom (about 60 sq m - 600 sq feet) for about USD$1800/month. Compared to big cities in the US, the rental price seems quite good for what you were getting.

-

I'm wrestling with this right now. I want to move to a nearby city, but have a great rate on my current house. So I'm leaning towards renting my current house out (I wouldn't break even, but close).

Still deciding if I should buy or rent the next house. Rent on a the next house seems like it'll be in the same ballpark as interest on a mortgage. Inventory on houses for sale where I'm looking is abysmal, I could rent for a few years, build a bigger downpayment and reassess. We'll see...

@xenon said in Rent vs. Buy -- math now favors Rent:

I'm wrestling with this right now. I want to move to a nearby city, but have a great rate on my current house. So I'm leaning towards renting my current house out (I wouldn't break even, but close).

Still deciding if I should buy or rent the next house. Rent on a the next house seems like it'll be in the same ballpark as interest on a mortgage. Inventory on houses for sale where I'm looking is abysmal, I could rent for a few years, build a bigger downpayment and reassess. We'll see...

You'd be fine, barring a bad recession, where you couldn't get the rent you needed or your renter couldn't pay. Then, it gets interesting.

-

That's right - I have to factor in the extreme downside risk (both renter and I lose our jobs). Need to make sure I have a good cushion to draw on. Seattle is notoriously tenant friendly.

@xenon said in Rent vs. Buy -- math now favors Rent:

That's right - I have to factor in the extreme downside risk (both renter and I lose our jobs). Need to make sure I have a good cushion to draw on. Seattle is notoriously tenant friendly.

We rented my house in the UK when we first came to Canada, but I found it was quite stressful. If somebody moves out, you can lose a month or two's rent, and that mortgage is still there round your neck like a horrendous albatross. If you've got free cash to tide you over you're probably ok, but we ended up selling the place as it was one less thing to worry about.

-

Couldn't read, due to paywall

Surely anybody who reads the Wall Street Journal can pay cash for their house?

@Doctor-Phibes said in Rent vs. Buy -- math now favors Rent:

Couldn't read, due to paywall

At $4 a month, I can afford it....

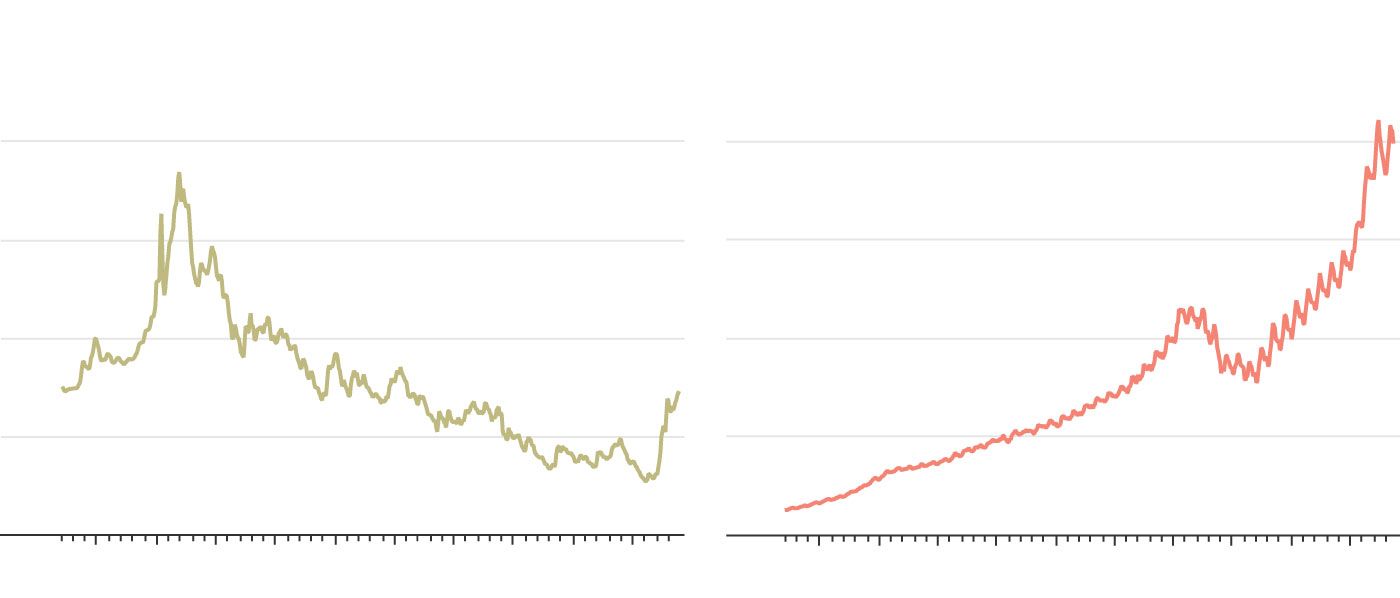

It is now less affordable than any time in recent history to buy a home, and the math isn’t changing any time soon. Home prices aren’t expected to go back to prepandemic levels. The Federal Reserve, which started raising rates aggressively early last year to curb inflation, hasn’t shown much interest in cutting them. Mortgage rates slipped to about 7% last week, the lowest in several months, but they are still more than double what they were two years ago.

Typically, high mortgage rates slow down home sales, and home prices should soften as a result. Not this time. Home sales are certainly falling, but prices are still rising—there just aren’t enough homes to go around. The national median existing-home price rose to about $392,000 in October, the highest ever for that month in data that goes back to 1999.

Average rate on a 30-year fixed mortgage, monthly

Median sales price on existing U.S. single-family homes

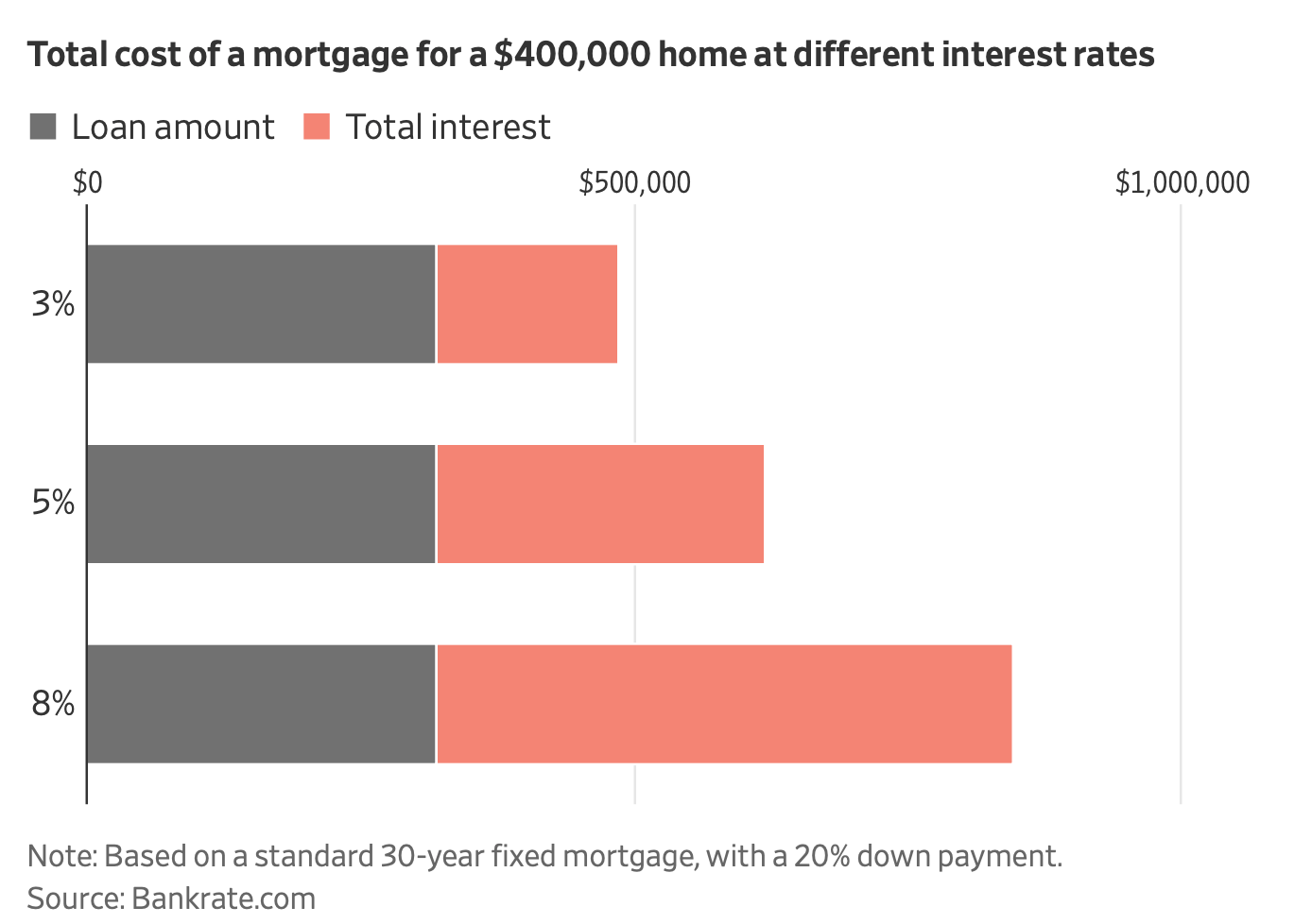

In mortgages, higher rates add up fast. An increase of just a few percentage points can mean hundreds of thousands of dollars more in interest over the life of a standard 30-year loan.

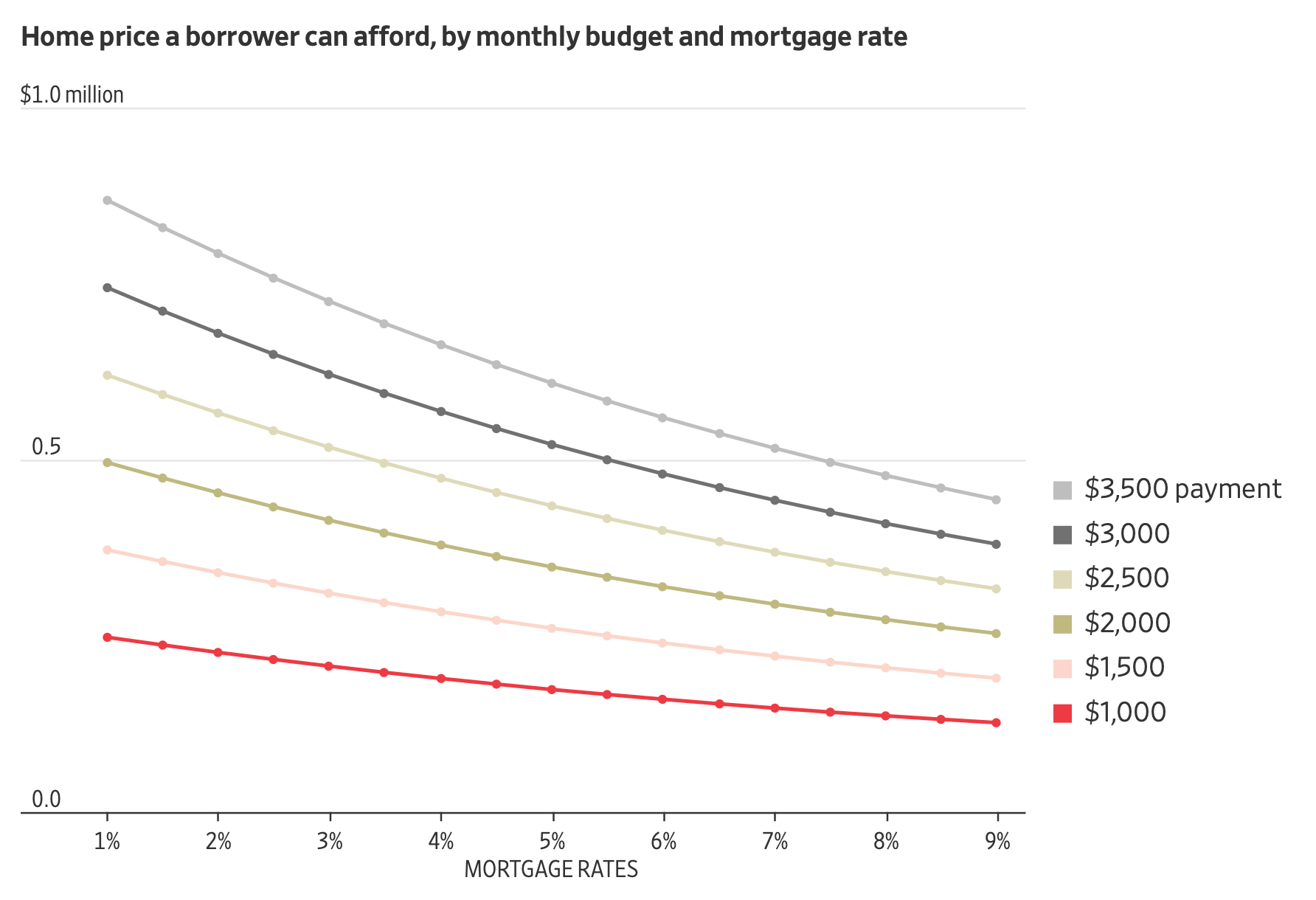

That means buyers get a lot less home for their dollar. Before the Fed started raising rates, a person with a monthly housing budget of $2,000 could have bought a home valued at more than $400,000. Today, that same buyer would need to find a home valued at $295,000 or less.

-

I'm wrestling with this right now. I want to move to a nearby city, but have a great rate on my current house. So I'm leaning towards renting my current house out (I wouldn't break even, but close).

Still deciding if I should buy or rent the next house. Rent on a the next house seems like it'll be in the same ballpark as interest on a mortgage. Inventory on houses for sale where I'm looking is abysmal, I could rent for a few years, build a bigger downpayment and reassess. We'll see...

@xenon said in Rent vs. Buy -- math now favors Rent:

I'm wrestling with this right now. I want to move to a nearby city, but have a great rate on my current house. So I'm leaning towards renting my current house out (I wouldn't break even, but close).

Still deciding if I should buy or rent the next house. Rent on a the next house seems like it'll be in the same ballpark as interest on a mortgage. Inventory on houses for sale where I'm looking is abysmal, I could rent for a few years, build a bigger downpayment and reassess. We'll see...

I'd say it depends on how long you plan to live in the next house. If for a while 15+ years, I would say buy. When rates come down, housing prices I'd imagine will only jump further. You can always refinance (or sell your previous place) if needed. If 10 years or less, probably just rent... gives you much more flexibility and you still have the income/equity of your current place. BUT WHY... that porch setting you built is awesome.

-

@xenon said in Rent vs. Buy -- math now favors Rent:

I'm wrestling with this right now. I want to move to a nearby city, but have a great rate on my current house. So I'm leaning towards renting my current house out (I wouldn't break even, but close).

Still deciding if I should buy or rent the next house. Rent on a the next house seems like it'll be in the same ballpark as interest on a mortgage. Inventory on houses for sale where I'm looking is abysmal, I could rent for a few years, build a bigger downpayment and reassess. We'll see...

I'd say it depends on how long you plan to live in the next house. If for a while 15+ years, I would say buy. When rates come down, housing prices I'd imagine will only jump further. You can always refinance (or sell your previous place) if needed. If 10 years or less, probably just rent... gives you much more flexibility and you still have the income/equity of your current place. BUT WHY... that porch setting you built is awesome.

@89th said in Rent vs. Buy -- math now favors Rent:

BUT WHY... that porch setting you built is awesome.

That's a whole other thread. I'm trying to get closer to my extended family (within 30min to 1hour to everyone). Right now I'm within 2-2.5hrs (without traffic - and there's often traffic).

I'd be making some pretty significant compromises to make that happen - but all in the spirit of spending more time with family/friends and giving my kids more of a sense of community (they have lots of cousins).

We also spend a ton of time many weekends driving back and forth. A lot.

Hello! It looks like you're interested in this conversation, but you don't have an account yet.

Getting fed up of having to scroll through the same posts each visit? When you register for an account, you'll always come back to exactly where you were before, and choose to be notified of new replies (either via email, or push notification). You'll also be able to save bookmarks and upvote posts to show your appreciation to other community members.

With your input, this post could be even better 💗

Register Login