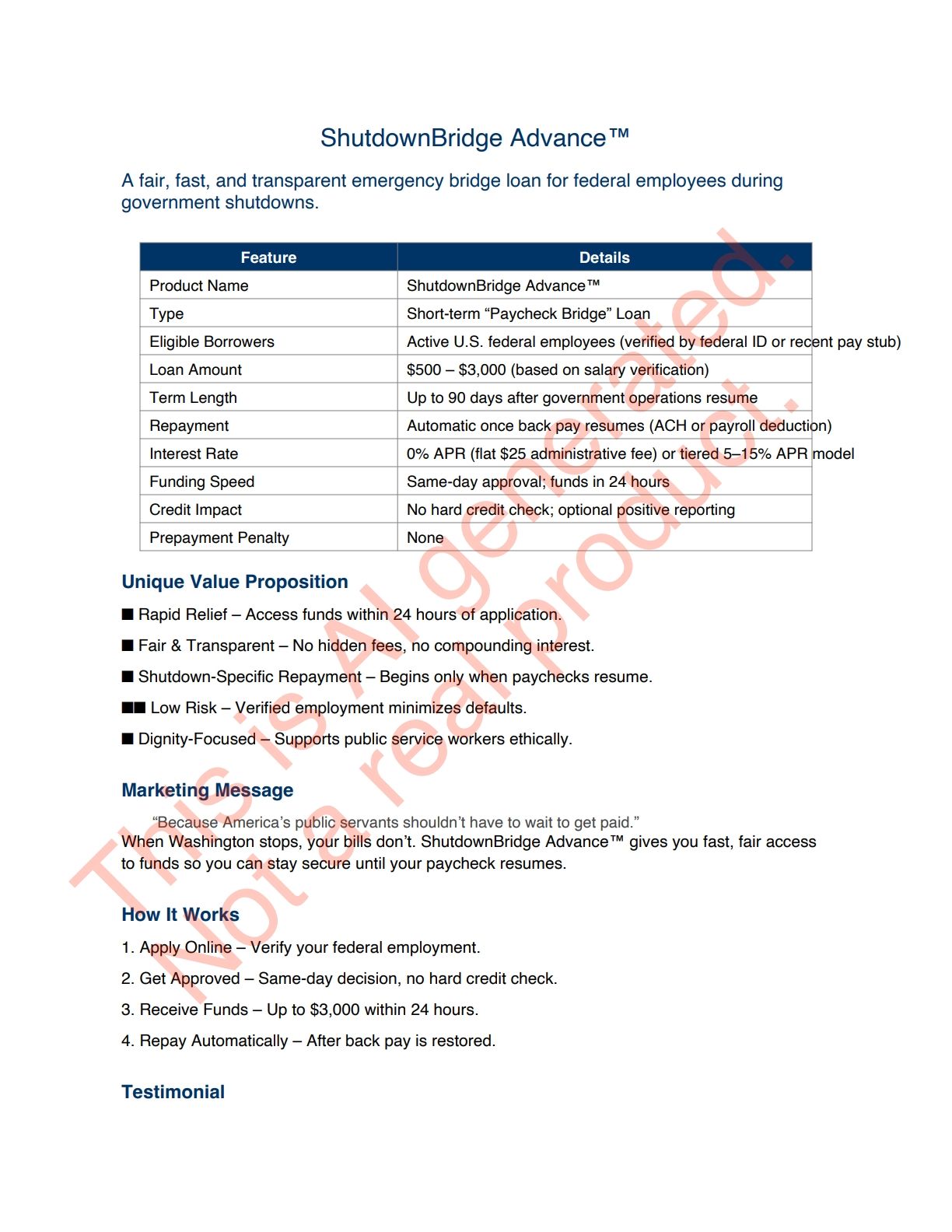

Payday Loans for Federal Government Employees?

-

That’s a very good — and nuanced — business question. Structuring and marketing payday-style financial products for federal employees during government shutdowns requires careful balance between financial need, compliance, and public perception. Let’s go step-by-step through both the product design and marketing strategy.

🧱 1. Product Structure

Federal employees affected by shutdowns present a unique risk and repayment profile — typically low default risk but temporary liquidity stress.

You can design products that address that specific pain point, distinguishing them from predatory payday lending.A. Loan Type: Short-term “Bridge” Advance

- Purpose: Cover missed paychecks during a government shutdown.

- Loan size: Typically $500–$3,000, depending on the borrower’s verified federal salary.

- Term: 30–90 days after the government reopens (not a fixed calendar date).

- Repayment: Automatically via ACH or payroll deduction once pay resumes.

B. Interest and Fees

- Position as a low-cost emergency advance, not a high-interest payday loan.

- Consider flat-fee or 0% interest with a small administrative fee — e.g., $25–$50 per loan.

- Alternatively, offer tiered APRs (e.g., 5–15%) depending on borrower’s tenure or credit score.

- Some credit unions offer 0% loans for up to $1,500 repayable over 6 months — that’s your competitive benchmark.

C. Risk Mitigation

- Require federal employment verification (e.g., recent pay stub or agency ID).

- Structure repayment to begin only once back pay resumes, reducing default probability.

- Optionally use group insurance or reserve funds to cover missed repayments if the shutdown persists.

D. Partnership Opportunities

- Partner with federal employee associations, credit unions, or nonprofits for credibility.

- Co-brand with “Federal Employee Relief Fund”–type initiatives.

- Banks or fintechs can use this as part of Community Reinvestment Act (CRA) outreach.

🧭 2. Marketing and Positioning

Government shutdown lending is politically and reputationally sensitive. The goal is to be seen as helpful and ethical, not exploitative.

A. Messaging Framework

Position as:

“A safety net for America’s public servants during uncertain times.”

Avoid terms like “payday loan” — use “emergency bridge loan,” “shutdown relief advance,” or “paycheck bridge.”

B. Channels

- Digital targeting: Paid search and social media ads aimed at federal workers (interests: “federal government,” “civil service,” “public employee unions”).

- Partnerships: Collaborate with federal employee unions (AFGE, NTEU) or advocacy groups for trusted distribution.

- PR campaigns: Focus on social good — e.g., “We stand with those who keep our government running.”

C. Timing

- Launch within 48 hours of shutdown announcement.

- Pre-market as a preparedness solution (e.g., “Sign up now for pre-approved shutdown support”).

D. Trust Signals

- Transparency: Clearly list costs, repayment terms, and eligibility.

- Offer financial literacy resources and budgeting tools — this builds goodwill and reduces regulatory risk.

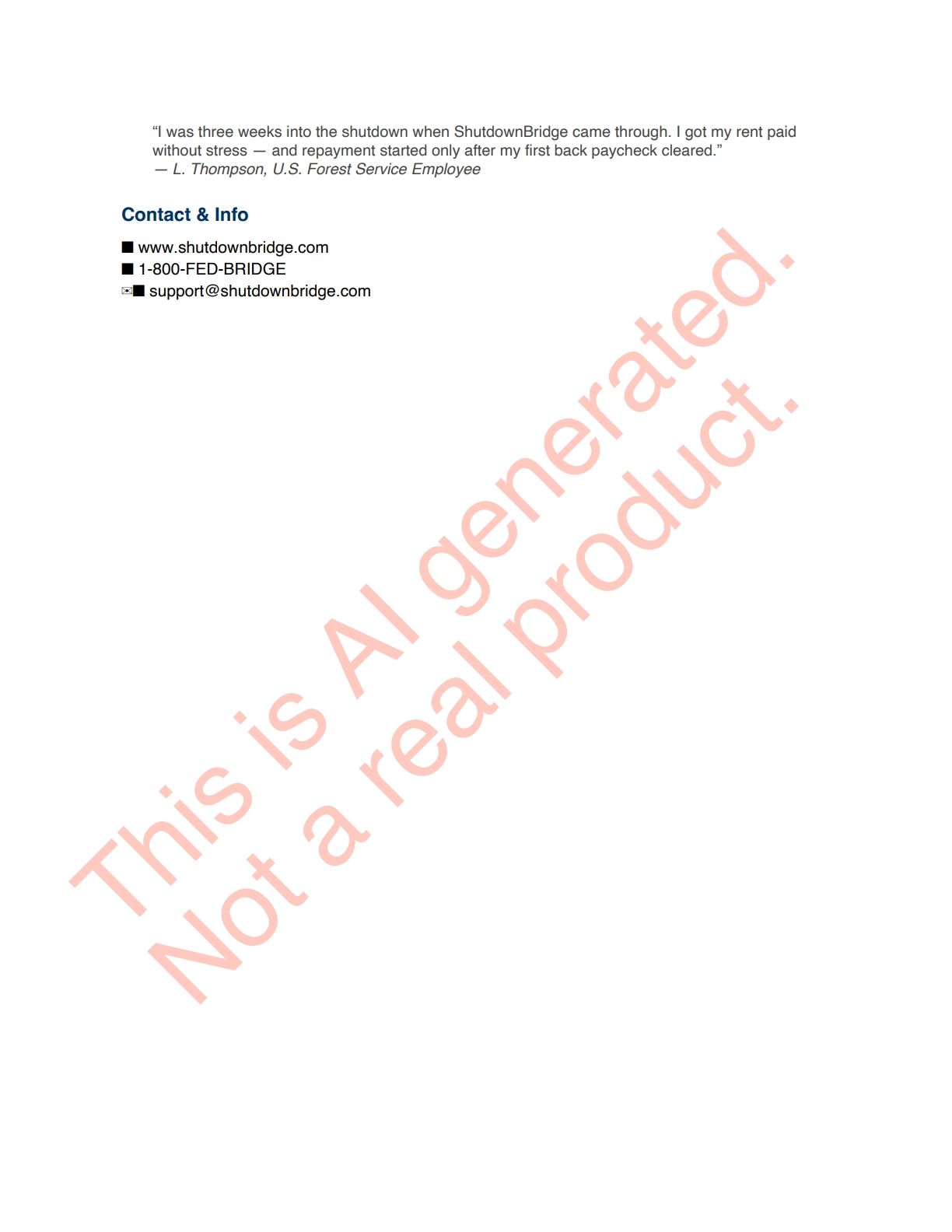

- Include testimonials from federal employees (if possible).

️ 3. Compliance and Legal Considerations

️ 3. Compliance and Legal ConsiderationsYou must ensure full compliance with:

-

Federal and state lending laws, including:

- Truth in Lending Act (TILA)

- Military Lending Act (if DoD civilians or active duty are borrowers)

- State usury caps and small loan laws

-

Avoid structures that could be construed as predatory or exploitative.

To stay compliant and credible:

- Register appropriately in all lending states.

- Disclose all fees and APR equivalents, even if positioned as a “service fee.”

- Avoid rolling over loans or compounding interest.

4. Differentiation and Expansion

4. Differentiation and ExpansionOnce established, you could expand into:

- Payroll-linked emergency savings programs (deduct small amounts per paycheck post-shutdown).

- Subscription-based access to low-cost advances (like a “safety fund” for federal employees).

- Employer-partnered relief plans where agencies or unions guarantee repayment post-shutdown.

Example Value Proposition

Example Value PropositionShutdownBridge Advance

- 0% interest for up to $2,000

- No payments until your paycheck resumes

- Designed exclusively for active federal employees

- Fast online approval — funds in 24 hours

This combines ethical intent, operational practicality, and solid marketing optics.

Would you like me to draft a sample product sheet and marketing one-pager (with name, features, terms, and compliant marketing copy)? That would show how to present it effectively to investors, regulators, or potential partners.

-

Need some cash, Ax?

-

https://www.csmonitor.com/USA/Military/2025/1010/shutdown-military-pay-gap

At the Army Community Center, where she provides financial counseling, Ms. Pena-Delgado says there’s been “a flood of soldiers” coming in for emergency pay loans. ...

... A quarter of service members have less than $500 in savings, according to advocacy organizations. ...

-

Wow, that’s going to be embarrassing when the military actually gets paid on the 15th.

Hello! It looks like you're interested in this conversation, but you don't have an account yet.

Getting fed up of having to scroll through the same posts each visit? When you register for an account, you'll always come back to exactly where you were before, and choose to be notified of new replies (either via email, or push notification). You'll also be able to save bookmarks and upvote posts to show your appreciation to other community members.

With your input, this post could be even better 💗

Register Login